Personal loans and overdraft against fixed deposits (OD against FDs) are two popular lending options available for individuals to meet their short or medium-term funding needs.

A personal loan is an unsecured loan that can be availed by salaried or self-employed individuals. The funds can typically be used for legal purposes, including debt consolidation, wedding expenses, home renovation, medical emergencies, or big-ticket purchases. Personal loans charge interest rates ranging between 10-25% p.a., along with processing fees up to 2-3% of the loan amount. The repayment is done through Equated Monthly Installments (EMIs) over a tenure of 1-5 years.

An overdraft against fixed deposits refers to a temporary credit limit sanctioned against an existing FD up to a certain percentage of its value (typically 80-90%). The credit limit can be utilized to withdraw cash from the FD account, allowing liquidity while keeping the deposit intact. The interest rate on an overdraft facility is 2-3% higher than the existing FD rate. Outstanding overdraft amount has to be settled in full before FD maturity to avoid breaking it prematurely.

Purpose of Comparison – Costs, Risks, and Benefits

This article compares personal loans and overdrafts against FDs across various parameters like interest rates, fees, loan amount, collateral requirement, repayment structure, credit impact, liquidity, risks, and total costs. As both options allow individuals to access funds and have varying pros and cons, weighing them based on costs, eligibility, risks, and benefits is important before deciding which works better for specific financial needs and situations.

The comparison will help assess key differences between the two instruments based on interest costs, processing fees, flexibility, liquidity, credit score impact, risk of default or non-renewal, and advantages related to each lending method. This will empower readers to make an informed choice after evaluating the pros and cons against individual priorities and payback ability.

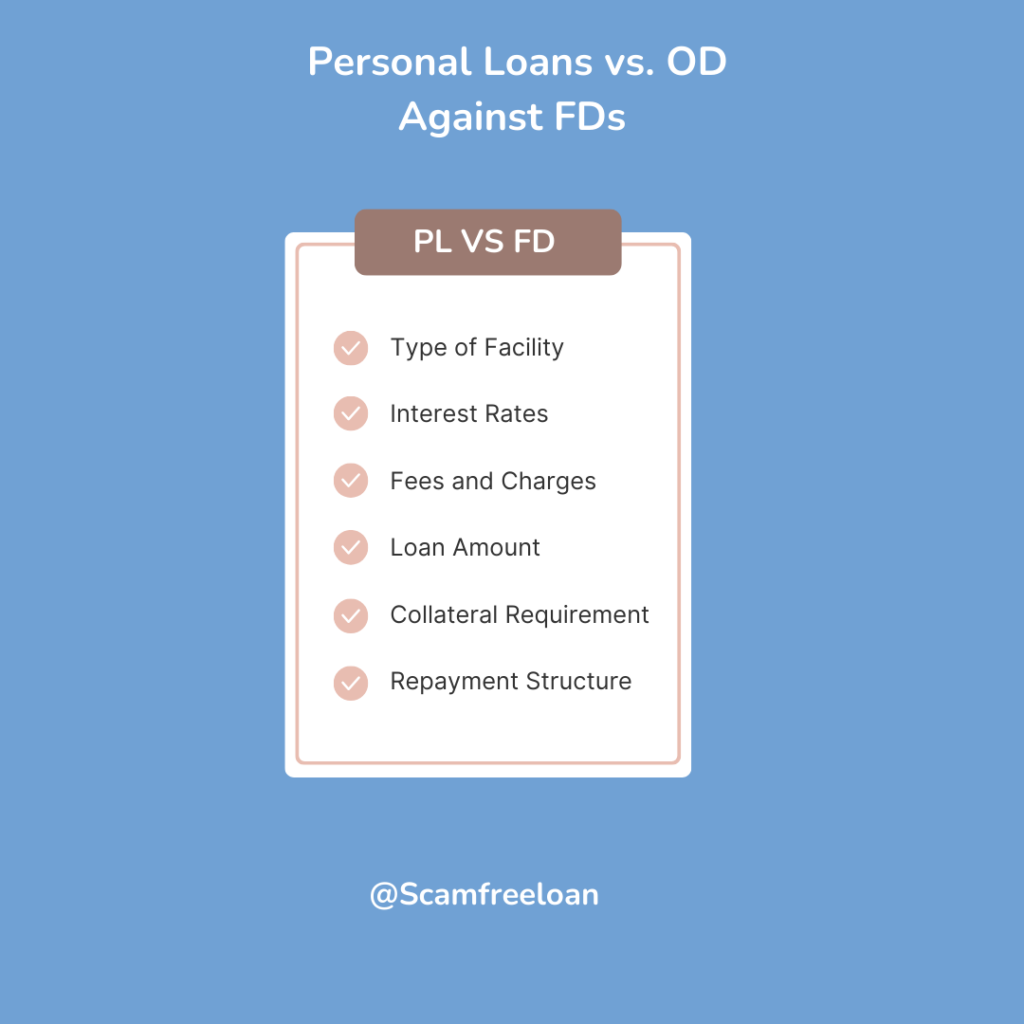

Key Differences Between Personal Loans and Overdraft Against Fixed Deposits

Here is a detailed comparison between personal loans and overdraft against fixed deposits across the requested parameters:

Type of Facility

Personal loans are general-purpose unsecured loans without any collateral requirement. An OD against FD is a secured credit facility provided specifically against an existing fixed deposit as collateral.

Interest Rates

Personal loans typically charge higher interest rates of 10-25% p.a. as they are unsecured. An OD against FD has interest rates of 2-3% above the FD rate, which makes it a cheaper source of credit comparatively.

Fees and Charges

While personal loans deduct up to 2-3% of the loan amount as a processing fee, an OD against FD only requires payment of a nominal documentation or renewal charge annually.

Loan Amount

Personal loans can approve higher loan amounts based on eligibility, even up to Rs. 25 lakhs for salaried individuals. The loan amount in case of an OD is restricted at 80-90% of FD value.

Collateral Requirement

No collateral or security is required for unsecured personal loans. Overdraft against fixed deposits uses the FD itself as security for availing the credit facility.

Repayment Structure

Personal loans repay in Equated Monthly Installments (EMIs) for up to 5 years. An OD against FD is an on-demand credit facility that has to be cleared fully before FD matures.

Also read – Get Easy Loans with Pradhan Mantri Mudra Yojana (PMMY) in India (Complete Process)

Personal Loans and OD Against FDs – Cost Comparison

Interest Costs

The total interest outgo on personal loans is higher owing to higher rates at 10-25% p.a. An Overdraft against fixed deposits only charges 2-3% above the FD rate; hence, interest costs are substantially lower.

Processing/Administration Fees

Personal loans deduct up to 2-3% of the loan amount as processing fees. An OD against FD only requires annual documentation charges of Rs. 250-500 for renewing the credit limit.

Early Closure Penalties

Pre-closing a personal loan attracts charges up to 5% of the outstanding amount. An OD against FD does not levy any foreclosure charges.

Renewal Costs

Personal loans may require paying renewal or re-issuance charges on ending loan tenure. An OD against FD only has nominal annual documentation charges.

Total Borrowing Cost

The aggregate of higher interest costs, higher fees, and penalties make personal loans a more expensive form of credit than an overdraft against fixed deposits.

Risks and Drawbacks – Personal Loans and OD Against FDs

While personal loans and overdrafts against FDs provide financing access, both options have potential downsides. Understanding the risks enables informed decision-making when evaluating these lending facilities.

Though offering more liquidity, personal loans and OD against fixed deposits also have negative aspects that must be weighed carefully before opting for either financing route.

Credit Score Impact

Availing of a personal loan can result in multiple hard inquiries, lowering credit scores temporarily. An Overdraft against fixed deposits does not impact credit history.

Loss of FD Returns

Opting for an OD against FD results in the deposit amount getting blocked while only earning interest rate minus OD rate. Returns are higher if the FD amount is kept intact.

Default Risks and Impacts

Defaulting on personal loan EMIs can severely lower credit scores and risk legal action. However, the inability to pay the OD amount can lead to the premature breaking of the FD.

Renewal Risks

Personal loans have minimal renewal risks unless major adverse credit events. However the OD limit may not renew if FD frequently requests premature withdrawal.

Benefits and Advantages – Personal Loans and OD Against FDs

Along with risks, personal loans and overdrafts against fixed deposits also present unique advantages that make them useful funding options for individuals’ needs. Highlighting the key benefits allows for a more holistic comparison between these facilities.

Amid the risks discussed, one should not overlook the positives of increased liquidity and flexibility provided by personal loans and overdrafts against FDs. Analyzing key advantages and benefits facilitates factual comparison.

Flexibility in Liquidity

Personal loans offer flexibility in loan utilization for any legal purpose. OD against FDs can only allow withdrawals from the FD account itself, limiting usage.

Possible Tax Benefits

Interest and principal repayments on a personal loan allow tax benefits under Section 80C and 80E up to certain limits. OD against FD does not offer tax benefits.

Lower Documentation

Personal loans require higher KYC and income documents for application processing. OD against FDs can be approved based on deposit statements and KYC.

Speed and Ease of Approval

An OD against existing FD can get approved quicker than personal loans depending on lender turnaround times after submission of documents.

Which One is Better for You?

With an overview of costs, risks, and benefits, the next key question is assessing which facility aligns better with individual financial situations and requirements. Choosing between a personal loan or overdraft against FD depends on certain personalized evaluation parameters.

Depends on Eligibility and Requirement

Customers with an existing FD find OD more suitable, while others may need to opt for personal loans purely based on eligibility. Loan amount requirement also plays a key role in facility choice.

Compare Total Costs

Assessing total borrowing costs across interest payout, fees, and foreclosure or renewal charges will present a clearer picture of cost efficiency.

Evaluate Risks Carefully

Understand the repayment capacities to avoid default on EMIs and risk of losing FD on inability to clear outstanding OD. Renewal risks also need evaluation before choosing an option.

Align with the Financial Situation

Analyze current income, cash flows, repayment ability, and risk appetite. Ensure to pick an option that aligns with financial priorities and needs.

Conclusion

The choice between a personal loan and overdraft against FD depends on multiple individual factors like eligibility, costs, liquidity needs, and risk capacities assessed through a combination of quantitative and qualitative analysis. While OD against FDs proves cheaper, personal loans offer greater flexibility, therefore, evaluate all pros and cons before deciding the most suitable lending option. Carefully studying terms across providers is also advised for the most competitive rates. Assess your financial situation diligently to pick the loan facility that fulfills your requirements.